Insight / Blog

Case study: What does InPost’s annual report tell us about lockers and out-of-home delivery?

Summary: See what’s working, what makes it different and what the future holds for the locker giant.

InPost is becoming something of a poster child for Out-of-Home (OOH) delivery, with an extensive locker network in Poland, recent expansion in the UK, and a major acquisition under its belt in the form of Mondial Relay. Its size and brand recognition make it a handy case study for both the role of OOH delivery more generally, and some of the core benefits it offers, as well as a useful example to analyse locker performance when considering the location mix of an out-of-home network.

So what can we learn from InPost’s most recent financial reports – what is working for the locker giant, what makes it different to other carriers and where will it need to go from here?

NB: InPost uses ‘lockers’ differently to how we might usually see the term used. It calls them APMs, or Automated Parcel Machines, and uses lockers to refer the individual compartments in parcel machines.

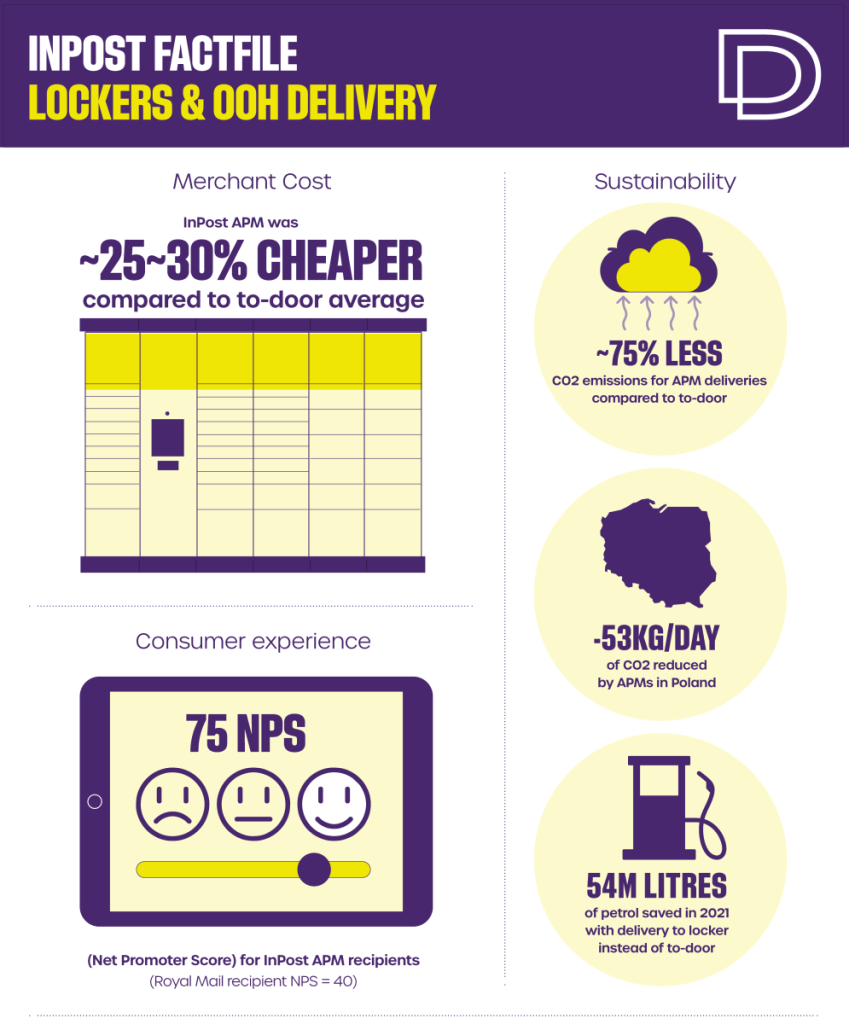

Factfile:

Text version:

Cost (to merchant)

-

~25~30% cheaper (InPost APM) compared to to-door average

Consumer experience

-

75 NPS (Net Promoter Score) for InPost APM recipients (for context, Royal Mail recipient NPS = 40)

Sustainability

-

~75% less CO2 emissions for APM deliveries compared to to-door

-

53kg/day of CO2 reduced by APMs in Poland

-

54m litres of petrol saved in 2021 with delivery to locker instead of to-door

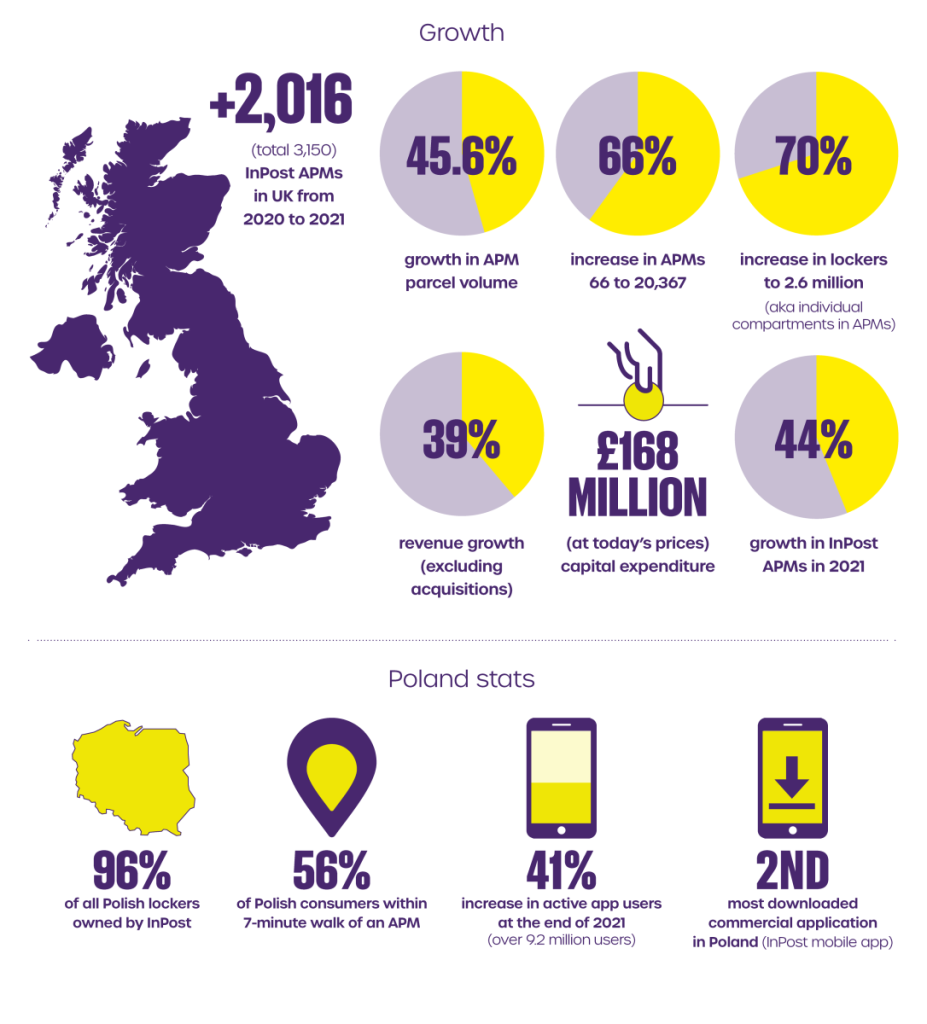

Growth

-

+2,016 (total 3,150) InPost APMs in UK from 2020 to 2021

-

45.6% growth in APM parcel volume

-

66% increase in APMs to 20,367

-

70% increase in lockers to 2.6 million (aka individual compartments in APMs)

-

39% revenue growth (excluding acquisitions)

-

£168 million (at today’s prices) capital expenditure

-

44% growth in InPost APMs in 2021

Poland stats

-

96% of all Polish lockers owned by InPost

-

56% of Polish consumers within 7-minute walk of an APM

-

41% increase in active app users at the end of 2021 (over 9.2 million users)

-

2nd most downloaded commercial application in Poland (InPost mobile app)

Density and differentiating on convenience

The annual report brings a lot of flavour to these numbers. Some highlights include the emphasis on density, based on the data showing that “consumers increase intensity of usage as their proximity to InPost lockers improves”. That echoes what Doddle has found in Japan working alongside Yamato and Quadient, where creating a truly dense network of parcel lockers enables Tokyo residents to pick up and drop off parcels within minutes. This behaviour quickly becomes habitual for users.

In the UK, InPost has been emphasising the label-free nature of its returns proposition, with QR codes powering item drop-offs into lockers. That is specifically designed to address the large and returns-intensive fast-fashion market in the UK, and some leading merchants in the space have partnered with InPost to enable this offering. Seeking to stand out on both sustainability and customer experience, leading on their own brand has been important for InPost’s reach in this space, with its logo on the websites of major retailers and its proposition earning valuable real estate in their returns policies.

While other label-free offerings have been in the market for some time (first brought to the UK by Doddle in 2014), the way InPost has used it to drive adoption and position itself as the top option on returns pages is certainly new, and aligns with its emphasis on customer experience in the proposition to merchants.

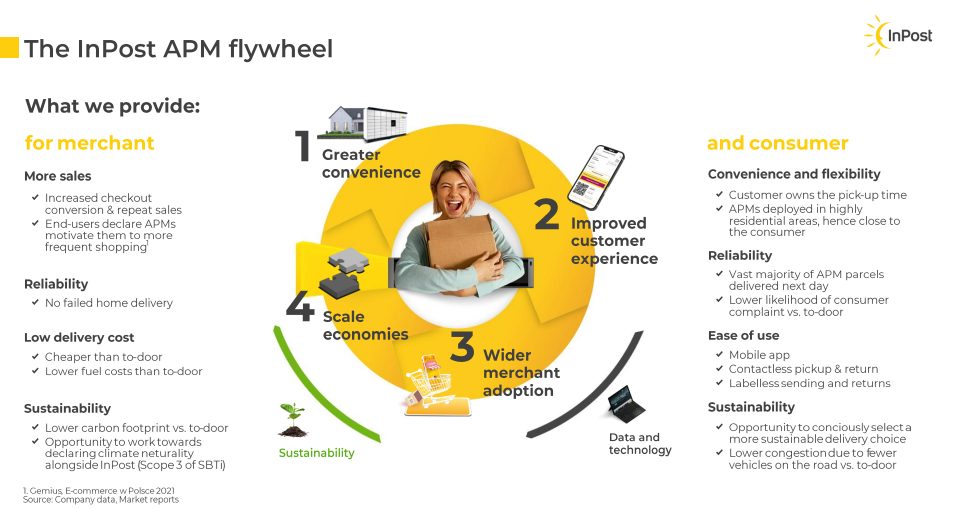

It’s here where InPost’s positioning is most markedly different from other carriers. As the slide shows, InPost sees its APMs creating an improved consumer experience, which translates to merchant benefits, as well as offering cost reductions, which drives further merchant business for InPost, which helps it to realise economies of scale, which in turn allows it to expand and create denser, more accessible locker networks. The financial resources at InPost’s disposal allows them to scale a network to attract greater merchant volume, getting them past one of the major ‘chicken and egg’ challenges of Out-of-Home delivery.

Flywheels are pretty popular in company results presentations these days, thanks to one Mr Bezos and his infamous example of the concept. However, in the carrier space, it’s rare to see a delivery proposition articulated in this way – which is a shame, because surely many or most parcel delivery businesses think along similar lines. Offering a markedly better and distinctive customer experience encourages merchants to use the service, which enables the service to improve and grow.

InPost’s clarity of thought here is partly because it is a younger, more technology-led business – and partly because its business is just simpler than say, a major national post which has to worry about letters and cross-border trade and a telecommunications arm, et cetera. Having such a simple way to articulate a differentiated proposition, though? That’s something more carriers could strive for.

Blending PUDO and automation

Unsurprisingly, the biggest priority facing InPost is integrating and adapting the newly acquired French PUDO business, Mondial Relay.

“The company is now focused on substantially elevating the Mondial Relay consumer experience, both through the existing PUDO network and via automation”

What’s interesting is that while at the time of the acquisition there was plenty of emphasis on automation, the language now reflects a mix of automation and the existing counter-based PUDO format. InPost plans to use its undoubted capabilities at rolling-out successful APM networks to adapt and partly automate an existing PUDO network, but whether it can realise a best-of-both-worlds scenario remains to be seen.

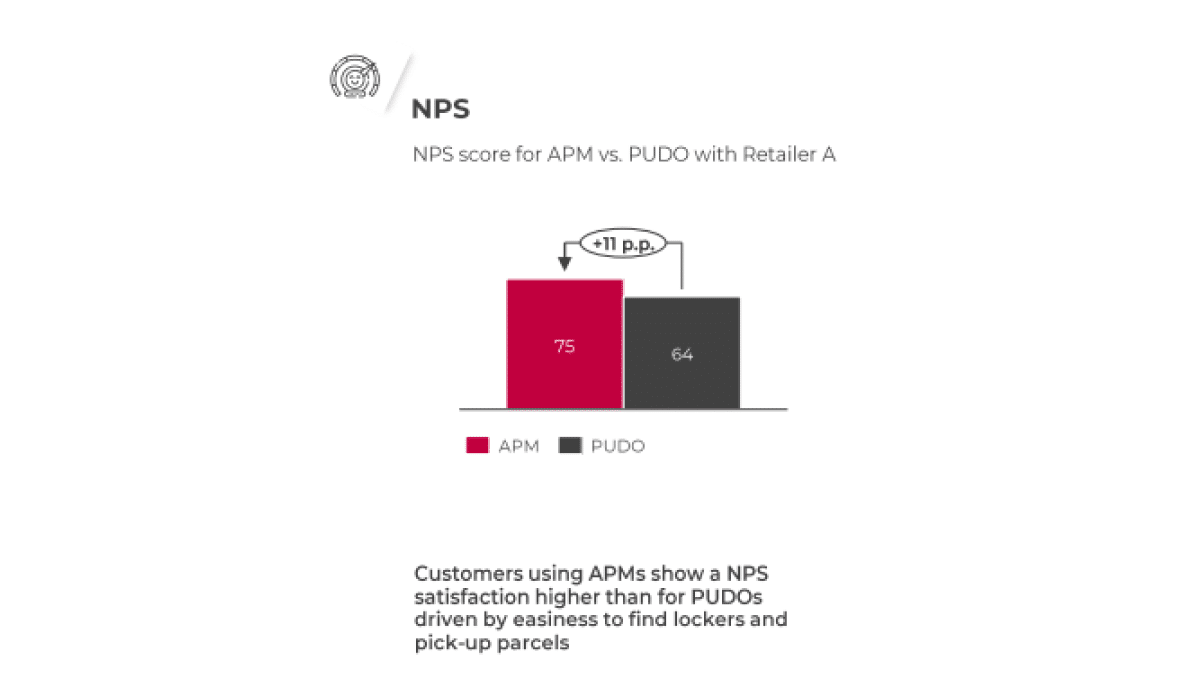

Some interesting comparison data from the report appears to back InPost’s decision to partly automate the Mondial Relay network. Net Promoter Score is higher for consumers using its APMs than PUDOs (75 vs 64), and parcel dwell time is under a day (0.9 days vs 1.3) for APMs compared to PUDO. The APMs also receive 25% more parcels per drop, which combined with the higher throughput from lower dwell times results in more network capacity – over twice as much (118% increase), according to InPost.

Why are parcel lockers so popular, and how do they compare to PUDO?

Expansion through partnerships

“Expanding partnerships is at the core of InPost’s European strategy”

With eBay and Vinted on board, InPost is looking at marketplaces and C2C as key areas to drive volume through the APM network and its Mondial Relay PUDO network . Lockers do appear to be a convenient solution for the fast-growing C2C market, with senders and recipients appreciating the 24/7 availability and security of lockers to conduct their transactions. It’s also worth noting that the power of InPost’s brand and ambition have probably played a role in its ability to close these deals with major marketplace players, who are often like-minded, tech-first entities.

Outside of Poland, InPost is more or less a new entrant looking at ways into competitive carrier markets, and being a fast mover on C2C and fashion returns provides it with a way to drive more volume into its network without necessarily becoming a major force on outbound volume, which is where the bulk of competition is. However, B2C outbound remains the dominant source of volume, which is why partnerships with merchants and InPost’s emphasis on convenience and NPS for consumers is still crucial.

The Out-of-Home Sustainability Advantage

“In Post lockers are already the most sustainable scaled solution for e-commerce last mile from a CO2 emission, fuel usage, and road safety perspective”

The reporting makes constant reference to sustainability, driving home the sizable emissions reductions achieved compared to home delivery. While the data behind them is not as transparent as it could be, it’s immediately clear that the benefits of consolidation result in far fewer miles being driven to deliver parcels to lockers.

The key question then becomes how consumers are able to access the network. It would be great to see more data on this in future reports. If consumers are chaining trips together when they visit the locker to collect a parcel, or if they’re using public transport/walking/cycling, the emissions reductions are likely to stay similar to those quoted by InPost. It’s in cases where shoppers drive specifically to the APM where the sustainability benefit can be eliminated completely, and indeed potentially worsened by the carbon cost of their driving.

Regardless of the specifics, InPost is putting sustainability at the forefront. If it can start to add hard data to checkouts and surface information to consumers about the carbon savings of their APMs, it should be able to significantly increase the volume driven through its network and win merchants who are eager to offer genuinely sustainable delivery.

Where next?

InPost has a huge opportunity. Its proposition stands out in the market, its brand is recognisable, and it can claim some major customer experience and sustainability bonuses over rivals. The challenge is now to persuade merchants that customers really will use out-of-home delivery when it’s available, and to expand their presence at checkouts in their key growth markets.

Partnerships such as those it now has with eBay and Vinted will help boost InPost’s volumes and crucially, its brand recognition among consumers. Whether this can translate into it owning significant shares of parcel volume in the UK and French markets in future remains to be seen, and depends on the appetite for continued investment and the evidence continuing to support its process of automation.

If those sustainability benefits can be more accurately and completely defined, then surfaced to customers through a checkout integration, we can expect to see InPost offered by more merchants in the coming year. The capability to compete against anyone on convenience, sustainability and cost makes InPost a force to be reckoned with.

Topics:

Head of Customer Strategy

Simon joined Doddle in 2020, following 10 years as a management consultant. He leads our Strategy & GTM team, working closely with customers and ensuring that our products are launched effectively in market and adopted. Simon has broad knowledge of first and last mile strategy but has particular expertise in Doddle's Digital Returns Kiosk

Related articles

20th March 2024

Lessons from a decade in the first and last mile

A decade as Doddle taught us some lessons - and Blue Yonder helps us see what will matter in the next decade.

12th February 2024

Parcel lockers vs parcel kiosks: which is best for parcel drop-off?

We explore the benefits and drawbacks of parcel lockers and kiosks to help decide the best self-service solutions.

8th February 2024

What do out-of-home networks look like in the UK?

We dive into the biggest logistics operators and their current OOH networks in the UK